If you’re planning to sell your home but decide to rent it out temporarily to offset expenses, it’s important to review your insurance coverage first. Many homeowners are surprised to learn that standard homeowners insurance typically does not cover rental situations, even if the rental is short-term.

Having the wrong policy in place can lead to denied claims and unexpected financial risk. Here’s how to properly protect both the property and yourself.

Why Homeowners Insurance Isn’t Enough

A traditional homeowners policy is designed for owner-occupied homes. Once a tenant moves in, the risk profile changes. If the insurance company isn’t notified and a loss occurs, coverage may be reduced—or denied entirely.

That’s why updating your insurance is essential before renting out the home.

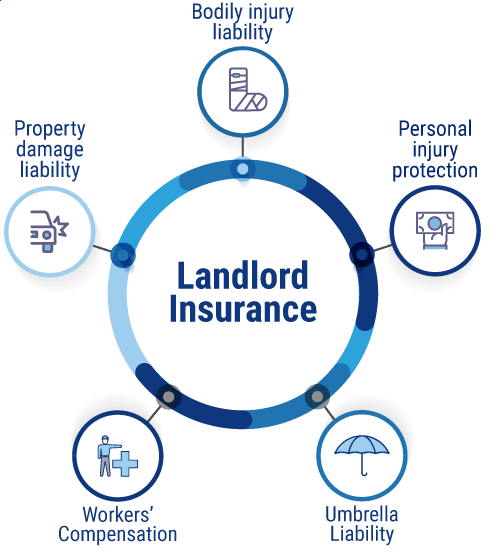

The Right Coverage: Landlord (Dwelling) Insurance

When a home becomes tenant-occupied, even temporarily, it should typically be insured with Landlord Insurance, often called a Dwelling Policy (DP-3) or Rental Property Insurance.

What Landlord Insurance Covers

1. The Structure of the Home

Coverage for damage to the building itself from covered risks such as fire, wind, storms, vandalism, and more.

2. Liability Protection

If a tenant or guest is injured on the property and claims negligence, landlord liability coverage helps protect against lawsuits and medical costs.

3. Loss of Rental Income (Optional)

If a covered loss makes the property uninhabitable, this coverage can help replace lost rental income during repairs.

What Landlord Insurance Does Not Cover

Landlord insurance generally does not cover a tenant’s personal belongings. For this reason, tenants should be encouraged—or required—to carry renters insurance.

Renters insurance helps cover:

- The tenant’s personal property

- Tenant liability if they cause damage

- Temporary living expenses if the home becomes uninhabitable

This protects everyone involved and helps avoid disputes.

Additional Smart Coverage Considerations

1. Umbrella Liability Insurance

An umbrella policy provides extra liability protection beyond the limits of the landlord policy and is especially useful for those with significant assets.

2. Full Disclosure to the Insurance Company

Always inform your insurer that:

- The home is tenant-occupied

- The rental is temporary

- The property is intended to be sold

Some carriers offer short-term landlord endorsements for transitional situations.

3. Vacancy Coverage

If the property may be vacant between tenants or while listed for sale, vacancy coverage may be necessary. Vacant homes often have limited or restricted coverage without it.

What to Do When the Home Is No Longer Rented

Once the tenant moves out:

- Coverage may need to switch back to a homeowners policy, or

- Convert to a vacant dwelling policy until the sale is completed

Failing to update coverage during this transition is a common—and costly—mistake.

Final Thoughts

Temporarily renting out a home can be a smart financial move, but it requires the right insurance protection. To avoid coverage gaps:

✔ Replace homeowners insurance with landlord insurance

✔ Carry adequate liability protection

✔ Require renters insurance for tenants

✔ Notify your insurer of any occupancy changes

A brief conversation with an insurance professional can help ensure you’re protected while preparing your home for sale.